Authors: Patrick Drury Byrne, Senior Director & Cross Practice Sector Lead, Ireland at S&P Global Ratings | Sandeep Chana, Director, Structured Credit/CLOs

Contributors: Lori Shapiro, CFA | Sylvain Broyer | Brian D. Luke, CFA | Marina Lukatsky | Yogesh Balasubramanian

Published: July 7, 2021

Liquidity across sustainable debt markets is steadily increasing as primary markets expand and interest grows in lower-rated credit sectors.

There are signs that sustainable bonds may be pricing at a premium in certain sectors, although it is difficult to isolate ESG factors.

Improved standardization within sustainable debt markets could bolster overall liquidity further, but higher financing costs and lower liquidity could impact issuers that fail to meet investors' ESG thresholds.

Greening monetary policy operations might not be an easy task, but options exist, and their implementation could accelerate the development of green liquidity, especially in the corporate bond space.

As issuers' needs to finance their environmental, social, and governance (ESG) objectives rise and sustainable finance debt issuance accelerates, this should augur well for the future growth and stability of sustainable debt markets. But can we find compelling evidence of increased market liquidity and a greenium--a premium for sustainable debt--within these markets? Furthermore, as central banks continue to play a pivotal role in global markets, how important will future policy decisions be in bolstering the liquidity of sustainable debt markets?

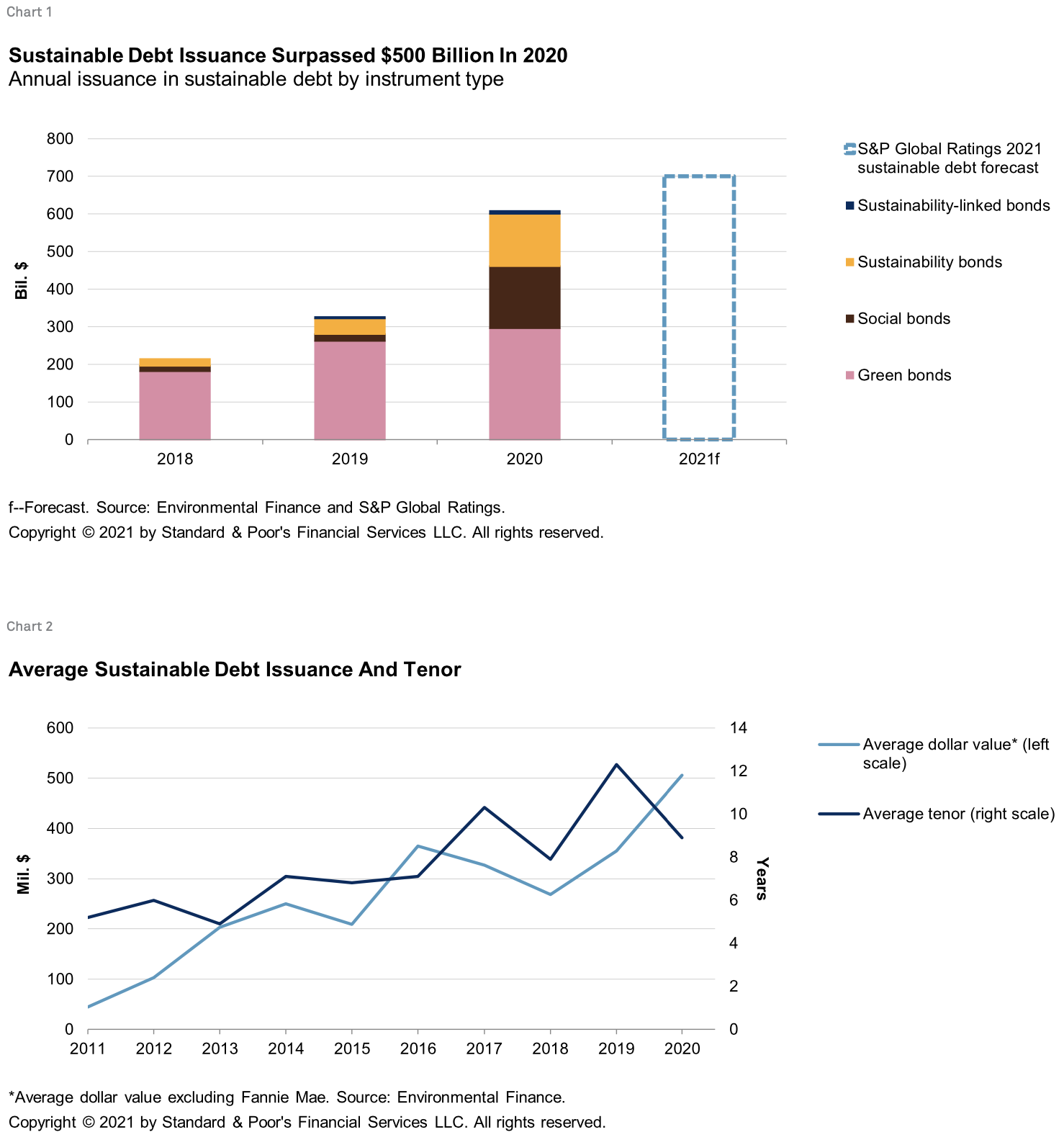

When evaluating the relative liquidity of a market, pricing is clearly a core component--and is certainly a hot topic within sustainable debt markets. But before we discuss pricing, it's important to explore the many other interrelated factors that play a significant role. Scale--in terms of issuance volume and product type--is a telltale sign of a growing market and increased liquidity. By both measures, the sustainable finance market has steadily grown over the last three years. S&P Global Ratings forecasts a 40% year-over-year increase in sustainable debt issuance in 2021 (see "Sustainable Debt Markets Surge As Social And Transition Financing Take Root," published Jan. 27, 2021). This level of growth is no small feat as it follows a significant growth rate of about 85% in 2020 (see chart 1). According to data from Environmental Finance, the average size of sustainable debt transactions has also steadily increased since 2011--a key trend since larger transactions are typically more liquid (see chart 2).

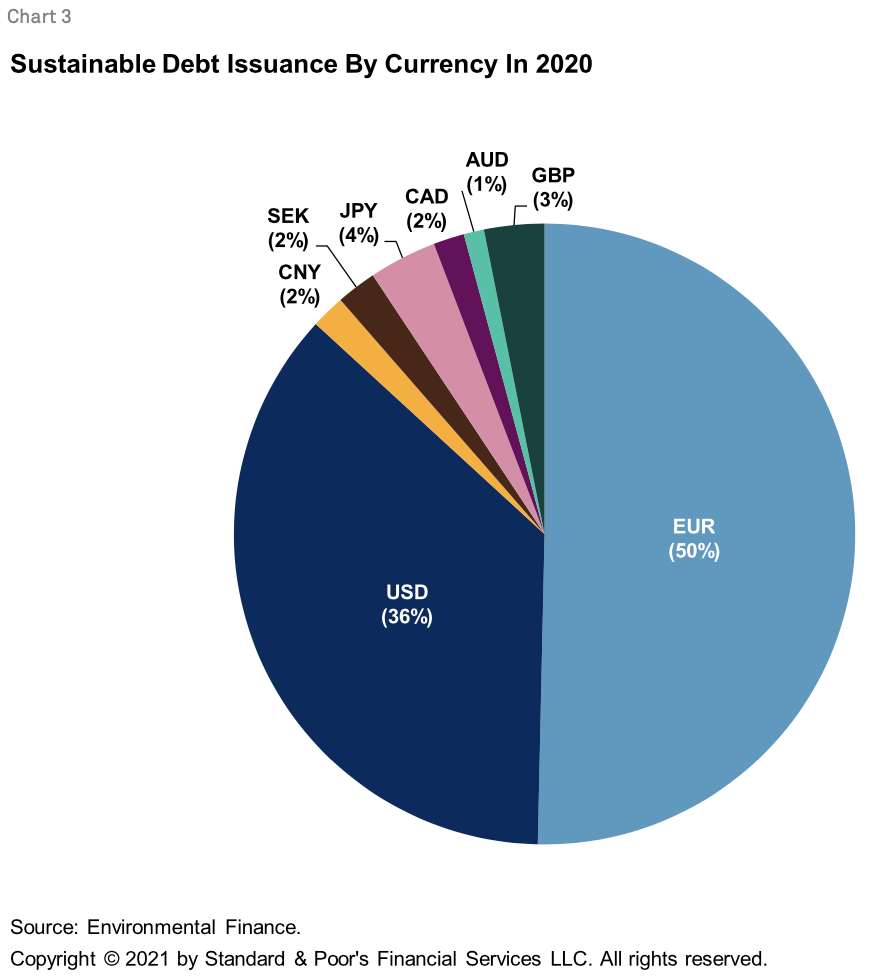

Another key sign of increasing market liquidity is the globalization of the market. Sustainable debt was issued in 32 different currencies in 2020 (see chart 3). While Europe and the U.S. are the dominant markets--and the euro and dollar the main currencies--it is noteworthy that the largest sovereign social bond in 2020 was issued by Chile, and the largest corporate social bond was issued by a Japanese company.

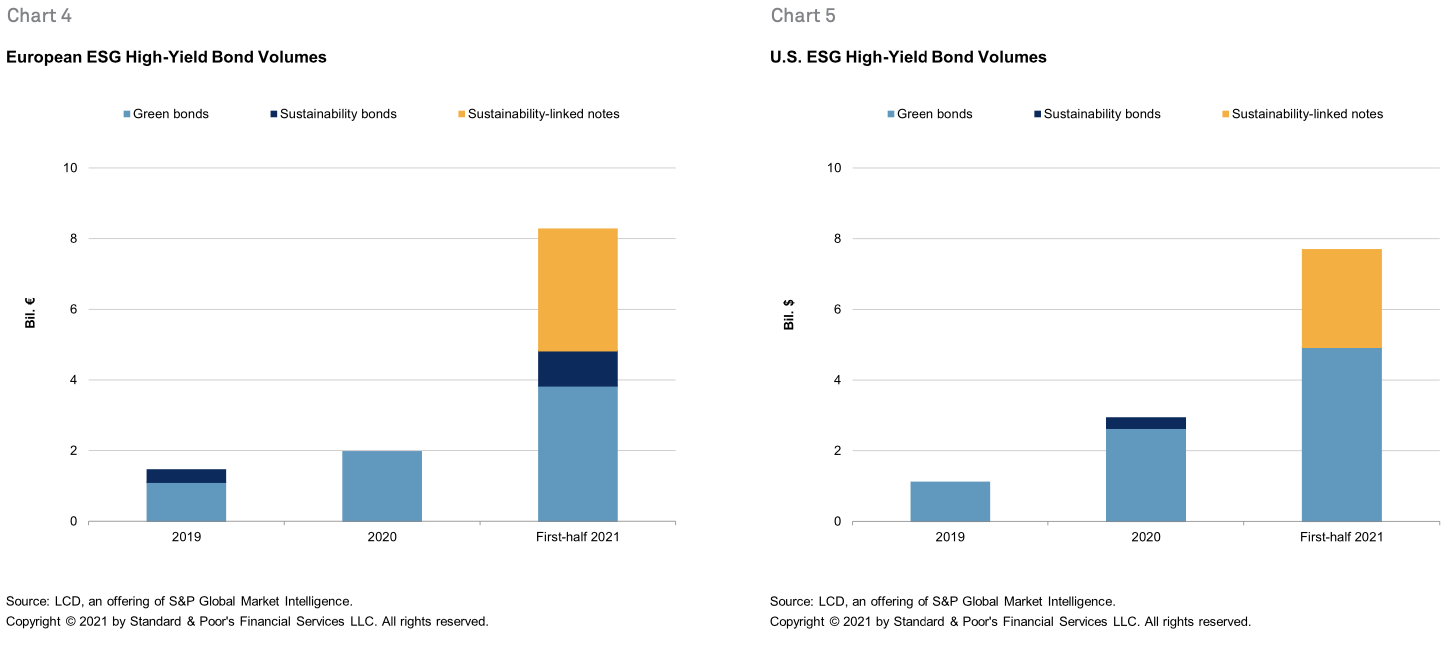

When we look closer at specific asset classes, there has been growth in some sectors that are lower rated and therefore arguably less liquid. According to a recent report by LCD, a division of S&P Global Market Intelligence (see "ESG Goes Mainstream Across Global Leveraged Finance Markets In 2021," published June 25, 2021), the European and U.S. high-yield bond sectors have shown strong year-on-year growth, in particular for sustainability-linked notes (see chart 4 and 5). Sustainability-linked notes have a step-up in coupon that is linked to ESG-related performance indicators. Interestingly, the step-up offers no pricing benefit to issuers if they meet their targets, only a penalty if they miss them. This approach differs from the European term-loan market, which does offer pricing benefits, and more than a quarter of European term loans now have a pricing mechanism with ESG language incorporated.

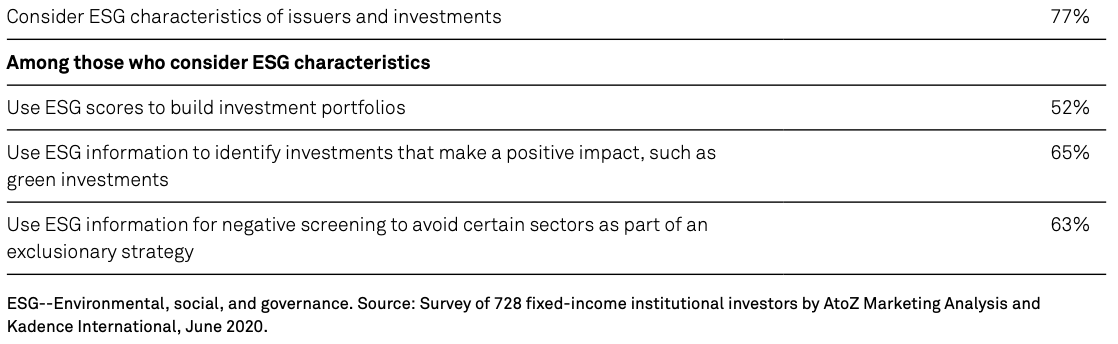

Increased market liquidity is also often correlated with increased investor demand. More investors are beginning to incorporate ESG themes within their investment mandates. A survey of 728 fixed-income institutional investors carried out by AtoZ Marketing Analysis and Kadence International in June 2020 reinforces this point (see table). According to respondents, 77% of investors consider the ESG characteristics of issuers and investments as part of their investment process.

Importantly, as the survey results highlight, investors' ESG strategies are not only limited to ESG characteristics, but also increasingly include elements of a socially responsible investment strategy. For example, investors may exclude investments that do not meet their ESG thresholds--arguably placing the burden of responsibility back on issuers. While this is a key trend in the evolution of ESG investing, it may over time unintentionally reduce liquidity as identifying, evaluating, and assessing ESG themes becomes clearer. A narrower approach over time may lead to fewer or more costly financing options and could result in less market liquidity for certain sectors that remain an important part of the global economy. Some sectors are already beginning to experience these challenges (see "The Energy Transition: ESG Concerns Are Starting To Present Capital Market Challenges To North American Energy Companies," published June 14, 2021).

Although liquidity within sustainable debt markets is growing, it is less clear whether financing cost benefits accrue to issuers of these instruments and whether investors are willing to pay a premium for sustainable bonds. Many macro and idiosyncratic factors influence bond pricing, which makes it difficult to isolate the ESG impact. However, without placing too much weight on any specific data point, data from different corners of the market suggests that there may be a pricing advantage for issuers that pass investors' ESG investment criteria.

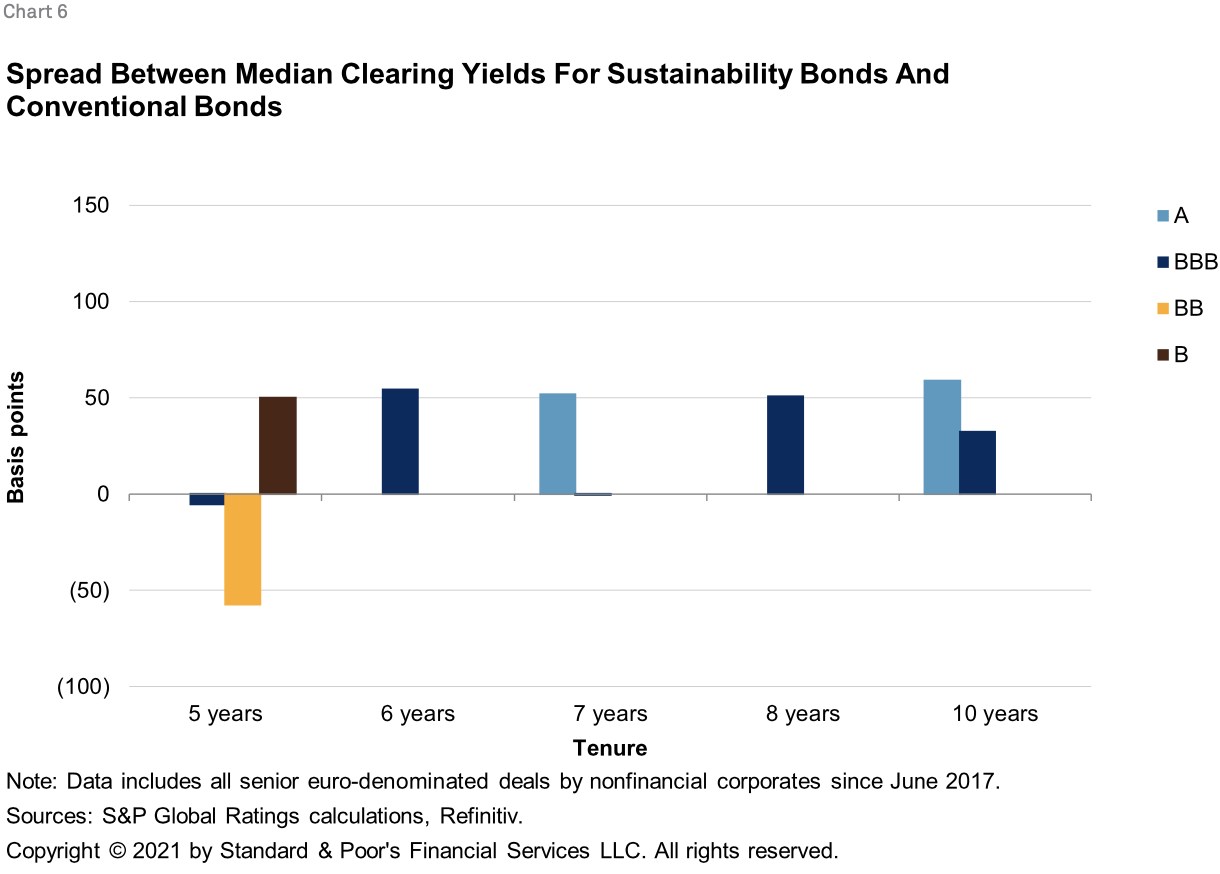

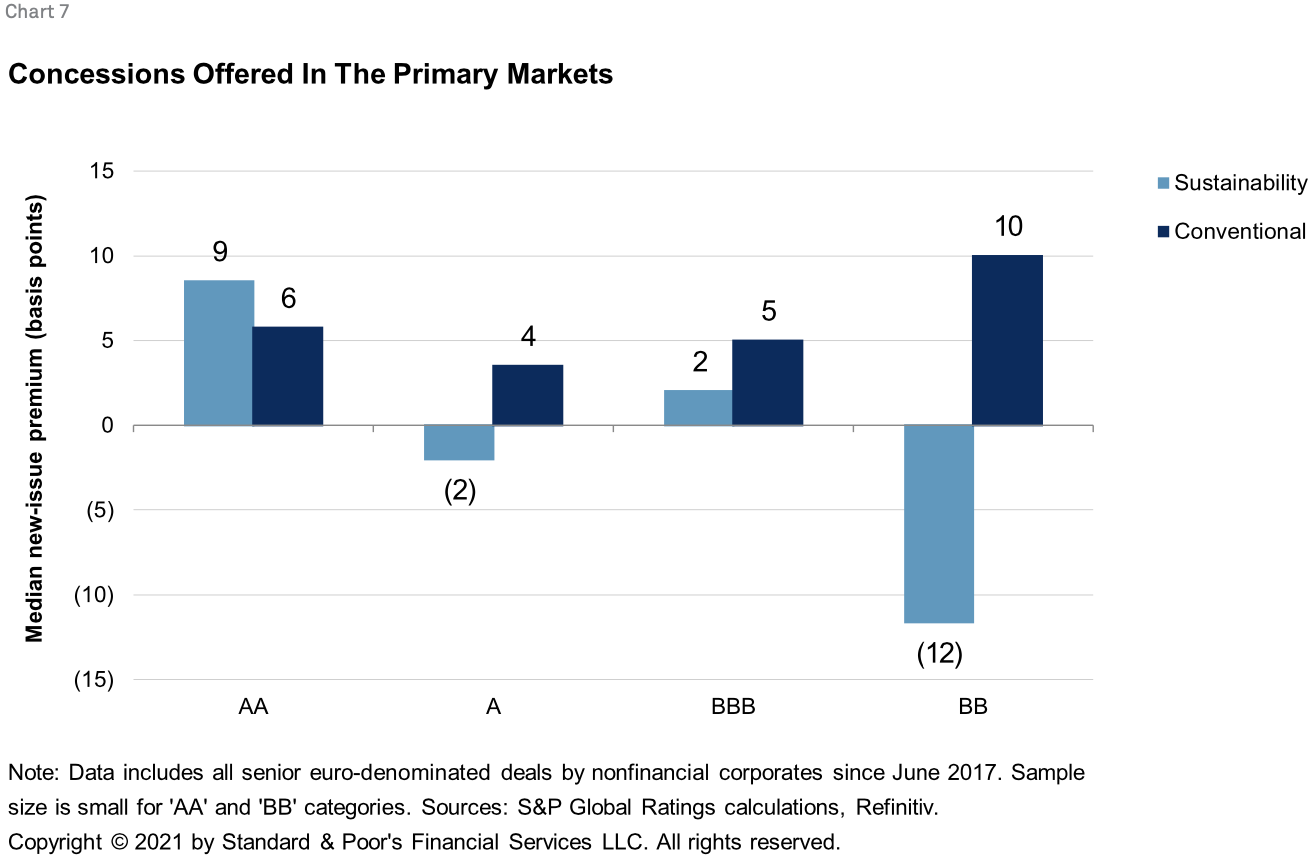

The clearing yield is a good place to start. Calculations derived from Refinitiv data suggest that, since June 2017, the median clearing yield for senior nonfinancial corporate sustainability bonds in Europe has been broadly tighter than for conventional bonds (see chart 6). Recent concession data for the same data set shows that concessions offered for European sustainability bonds are broadly lower than for conventional bonds--particularly at lower rating levels (see chart 7).

While many non-ESG factors also influence clearing yields, the same trends seem to hold, at least anecdotally, in parts of the market that would typically be less liquid. According to a report from LCD, "Sustainability-Linked Bonds Offer Pricing Perk For Right Credits," published May 27, 2021, anecdotal evidence suggests that initial demand for sustainability-linked transactions in the European speculative-grade market could be 30%-40% greater than for conventional bonds. This is because investors with multiple funds are placing larger orders, rather than a higher number of orders.

The strong demand for sustainable instruments relative to a still-limited supply has translated into favorable financing costs for some issuers. According to LCD, for instance, Europe's first sustainability-linked, speculative-grade bond deal--a €650 million issuance by Greece's Public Power Corp. S.A.--priced in March to yield 3.875%, while senior notes for similarly rated issuers have averaged a yield of 4.890%. There is also some anecdotal evidence to suggest that CLOs with documented ESG requirements may appeal to a wider investor base than traditional CLOs, with lower clearing yields particularly for lower-rated tranches.

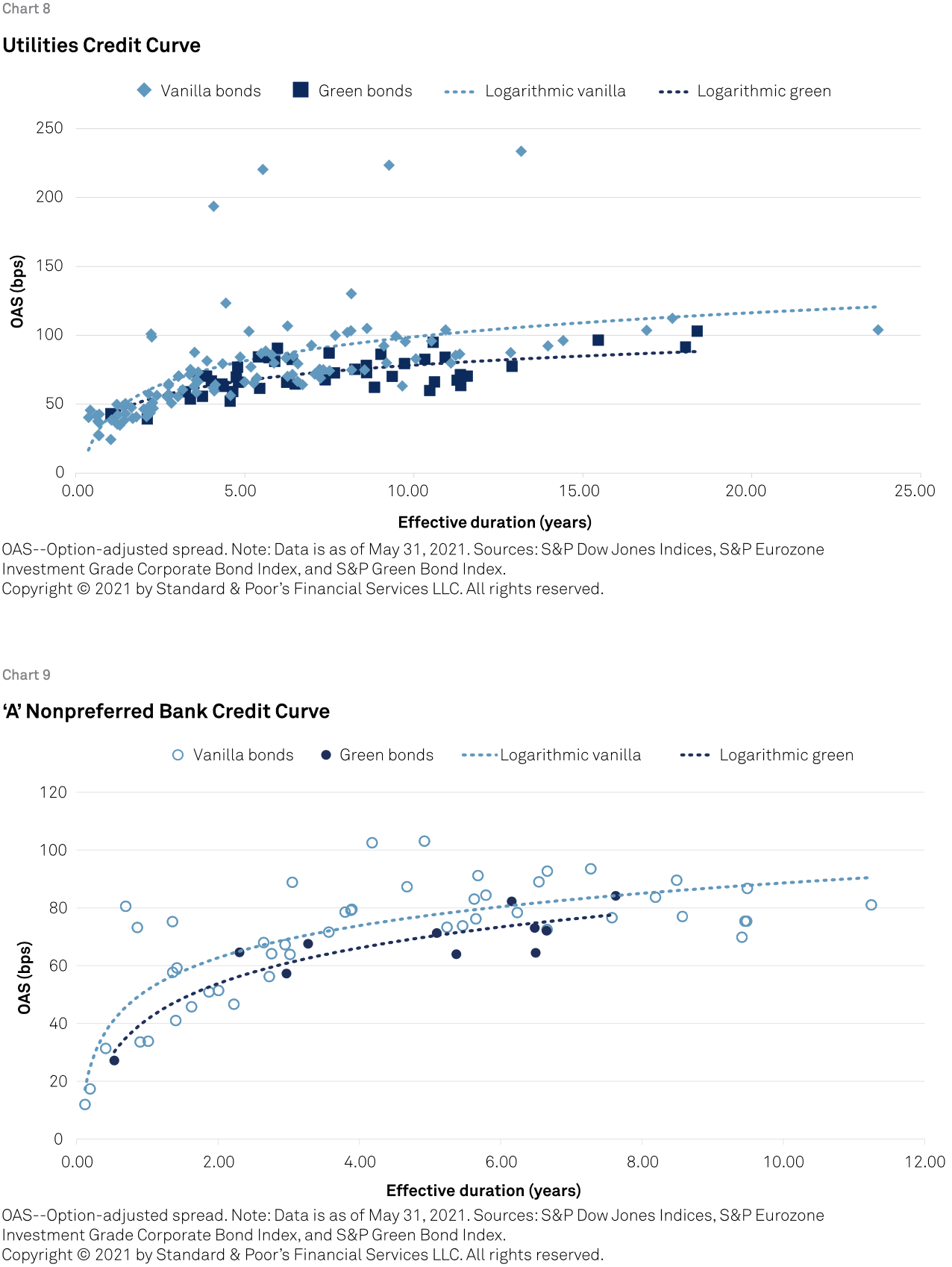

More compelling evidence supports the presence of a greenium, at least in certain sectors. An analysis by S&P Dow Jones Indices (SPDJI) sought to isolate and highlight a investor greenium by constructing credit curves of similar bond issuance. First, SPDJI constructed a credit curve evaluating over 100 conventional European utilities bonds against 46 green bonds (see chart 8). Evidence of investors paying a premium for green bonds across this sector is apparent, illustrated by the lower yield offered. Spread deviation for vanilla bonds in the sample is significantly higher than that for green bonds, contributing to an overall higher curve. For example, the largest deviation of spread among green bonds is approximately 20 basis points (bps), compared to 120 bps for vanilla bonds. SPDJI also did a similar analysis using a sample pool of European senior bank debt with an index rating of 'A' (see chart 9). The results show similar patterns: a small premium with tighter dispersion across the sample size.

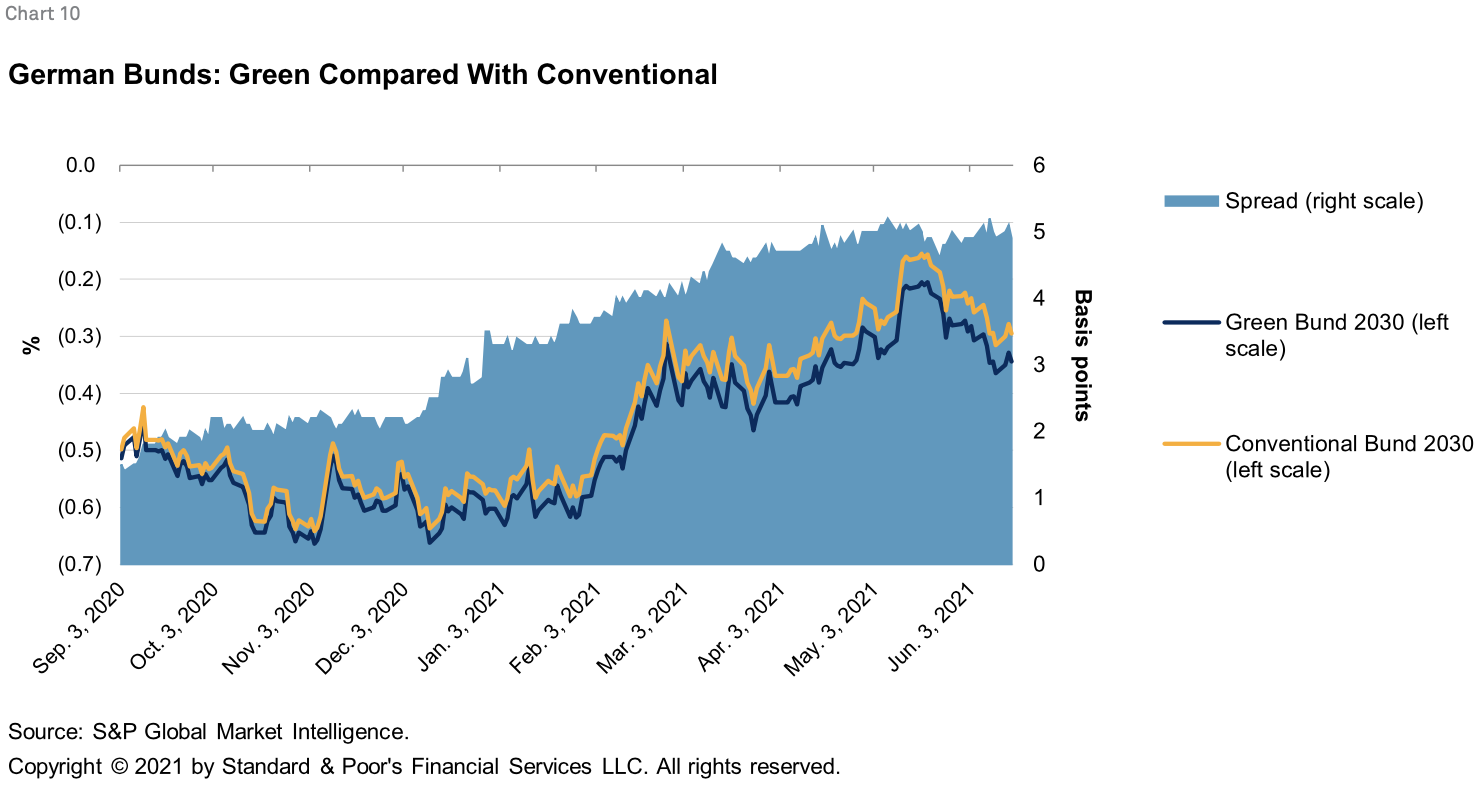

The spread differentials between German green bunds and conventional bunds also support the presence of a greenium in certain sectors. Green bunds trade at a premium to conventional bunds with similar maturities. While small, the differential is apparent and relevant given that duration and credit risk have been removed from the pricing equation.

All of these examples suggest that a greenium may be present in certain sectors, providing a pricing benefit to issuers who can demonstrate the required ESG credentials, but this evidence is not definitive given the various factors that influence bond pricing. Furthermore, liquidity in sustainable debt markets is unlikely to approach the levels of conventional markets until the sustainable debt markets make further progress in addressing its key challenges. The more transparent and comparable a market is, the more liquid the instruments are likely to be.

Progress in standardizing data, product standards, and reporting may improve transparency in the sustainable finance market. For example, there may be momentum from the EU's Taxonomy Regulation, which determines what constitutes a sustainable investment in Europe (see "A Short Guide to the EU's Taxonomy Regulation," published May 12, 2021) and from the new Article 8 and 9 sustainable investment product designations under the EU's Sustainable Finance Disclosure Regulation (see "What Is The Impact Of The EU Sustainable Finance Disclosure Regulation (SFDR)?" published April 1, 2021). Additional sustainable investment labels are expected in the EU, which will be directly linked to the Taxonomy Regulation, such as a new EU Green Bond Standard.

Individual stakeholders in the market seeking to tighten standards to avoid the risk of greenwashing will also contribute to greater transparency. For instance, according to LCD, the European Leveraged Finance Association and the Loan Market Association are working together on guidelines to ensure that market participants incorporate ESG provisions in an effective and appropriate manner, as pricing mechanisms linked to ESG performance become more prevalent. As issuers' needs to finance their ESG objectives rise and sustainable debt markets continue to grow, the more important it will be to create a level playing field for issuers and investors.

As central banks hold sway over current financing conditions, understanding their future role is becoming increasingly important to sustainable debt market participants. The role of monetary policy in addressing and mitigating climate change is a complex undertaking--and one that is evolving quickly. Whether monetary policy should play a role is no longer a matter of debate. Instead, the prevailing view is that central banks must act in unison with fiscal authorities, regulators, and supervisors, as climate stability is a prerequisite to financial stability and thus to price stability. The question of whether the legal mandate for central bank's independent inflation-targeting allows them to address climate challenges--a critical question for the European Central Bank (ECB)--has also been settled. Now, the question is how can monetary policy effectively be greened.

This needs to be handled with care. Central banks will need to find the right balance of policy instruments to deliver on the primary mandate of price stability on one hand, while mitigating their balance sheet risks and supporting the green transition on the other. This is necessary to avoid falling "from green neglect to green dominance," as Isabel Schnabel, Member of the Executive Board of the ECB, said in a speech this year. In a recent study, a group of experts from the Network for Greening the Financial System (NGFS), a network that currently represents more than 80 central banks and financial supervisors worldwide, concluded that four avenues look the most promising in meeting their stated objectives. The four options consist of tilting asset purchases toward climate-friendly assets, implementing a positive screening strategy, aligning the pool of collateral to climate factors, and adjusting the price of lending operations to reflect the counterparties' climate-related lending (see Related Research for more information).

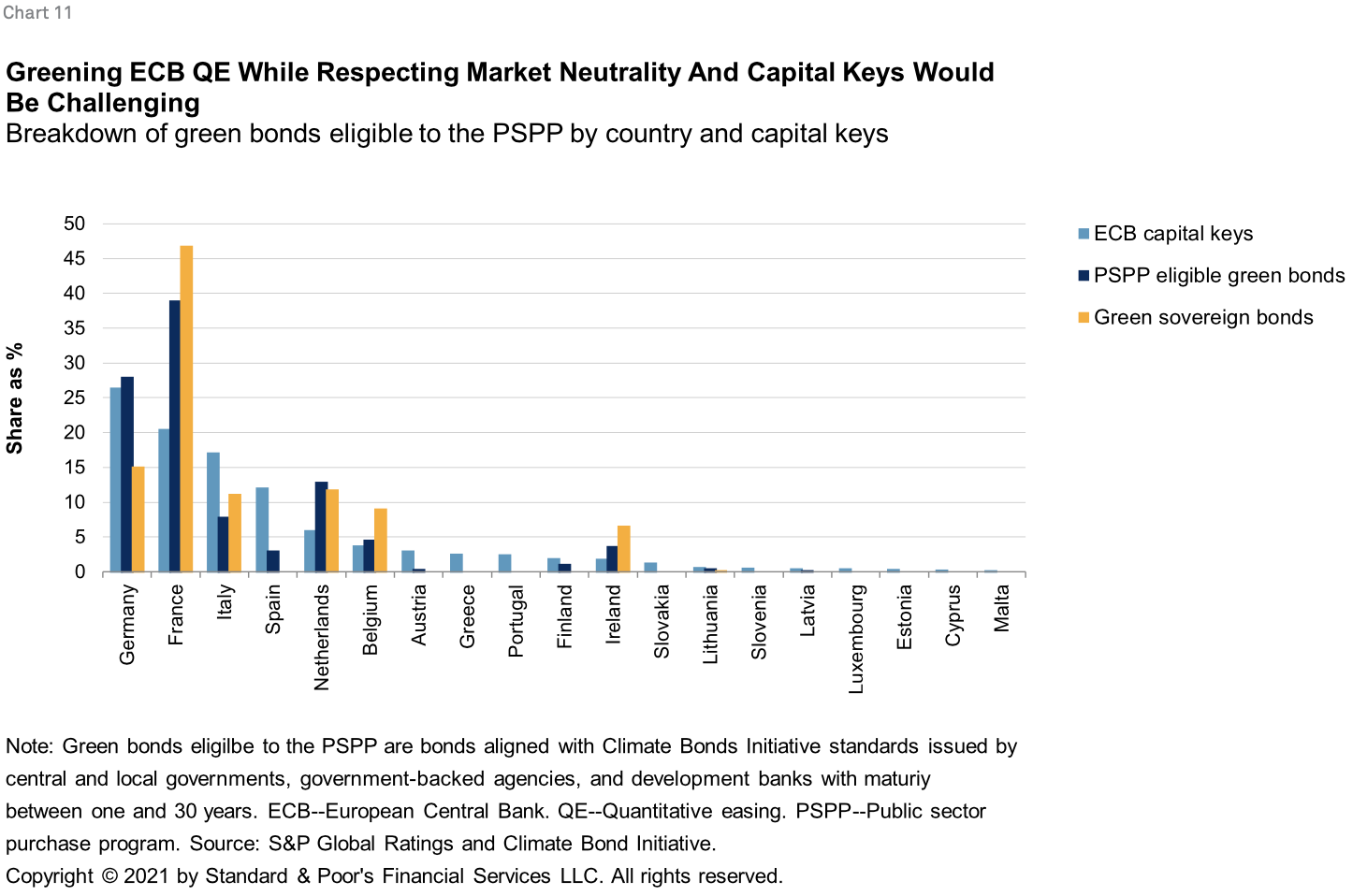

That said, no option provides a silver bullet, and the four avenues are not yet totally practicable. Some roadblocks still include issuers' and lenders' incomplete disclosures of climate-related exposures and the limited--although growing--supply of green financial assets. What's more, not all four avenues are equally practicable to all central banks. For the ECB, tilting public sector bond purchases toward green bonds will be challenging because the ECB also needs to respect the capital allocation keys. Even the pandemic emergency purchase program (PEPP), which is supposed to be flexible in this respect, does not deviate much from the capital keys. This may be because of the provisional nature of the PEPP and the need to eventually bring it in line with the public sector purchase program (PSPP) guidelines. The supply of green public sector bonds that are eligible to quantitative easing (QE) does not match the ECB's capital keys (see chart 11). Respecting market neutrality while purchasing green bonds that are eligible to the PSPP would lead the ECB to overweight French debt. The EU's issuance of green bonds as part of its Next Generation EU plan financing could help the ECB meet the capital key guidance, should the ECB maintain this guidance for the PSPP in the future.

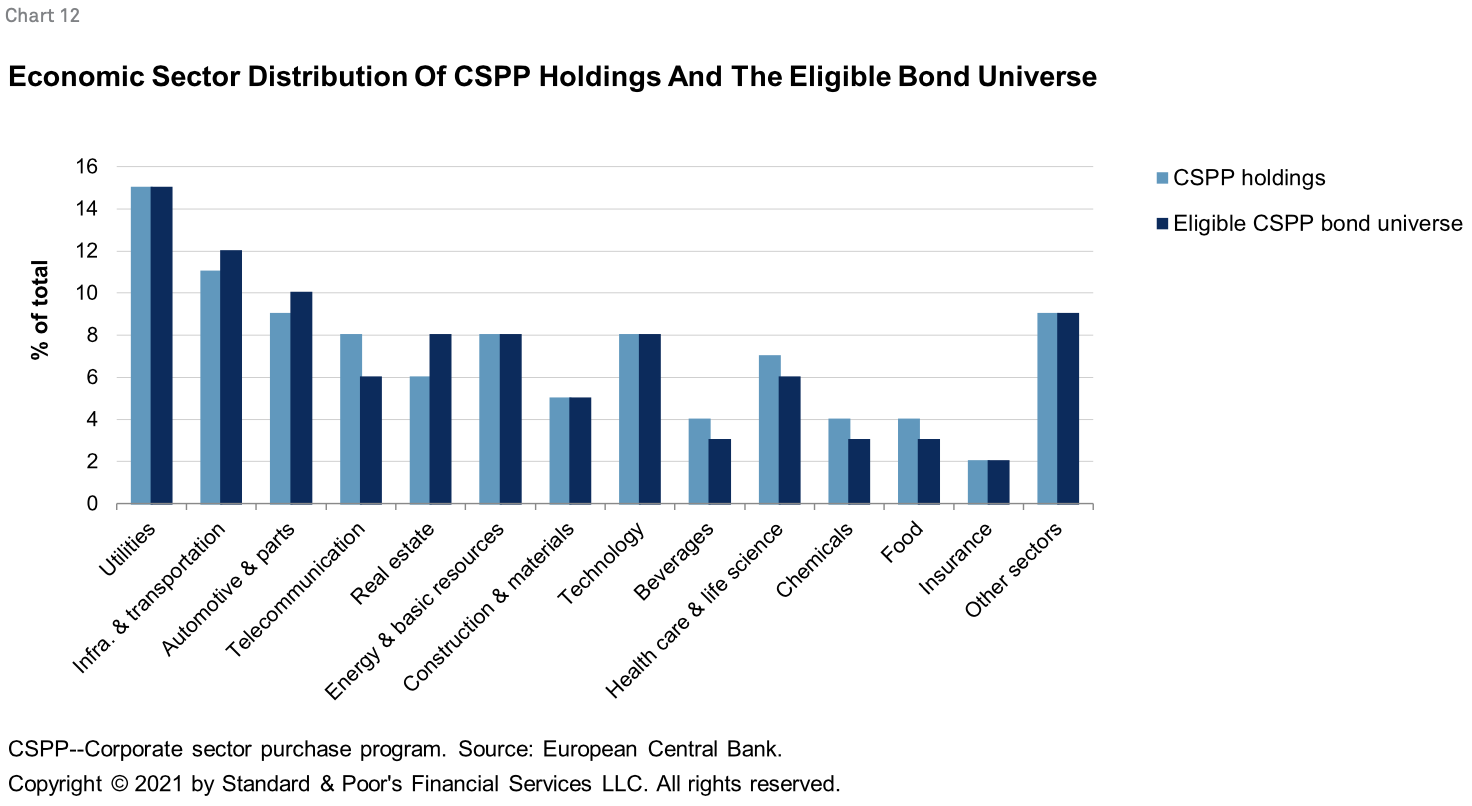

For these reasons, tilting corporate bond purchases may offer a simpler way to green ECB's monetary policy, but this would not be without challenges. The first hurdle is that the corporate sector purchase program (CSPP) does not make up more than 8% of bonds held by the ECB for monetary policy reasons. What's more, we estimate that a bit less than 7% of the portfolio of corporate bonds held by the ECB are included in the Climate Bonds Initiative database for green bonds. Conventional bonds are likely to dominate CSPP holdings and purchases for some time (see chart 12), even if the ECB overcomes the principle of market neutrality on this QE program, as Philip Lane, the ECB chief economist suggested on a panel recently. That said, tilting the CSPP toward green bonds would be a signal for financial markets, which might help foster and accelerate their greening.

The future of sustainable debt looks bright, and liquidity is steadily improving. Further progress will largely depend on the standardization of data, product standards, and reporting, as well as the decision-making of key stakeholders, including central banks. As ESG and credit markets become even more interdependent, the importance of fully functioning, liquid sustainable credit markets will only increase.

The authors would like to thank Aude Guez for research support on the section titled The Path To Greener Monetary Policy.