The uptake of electric vehicles varies across global economies, but the market is dynamic, and trends can change quickly.

Published: January 10, 2024

Electric vehicles are gaining market share, although affordability and ease of public charging remain challenges to broader consumer acceptance.

The share of EVs in the global light vehicle market will expand significantly over the next decade, driven by tightening government regulation.

Supply of battery raw materials is a key risk to a steep EV adoption curve.

EVs will erode oil’s near-monopoly as a road transportation fuel over time.

The global electric vehicle market has grown over the past three years, led by earlier adopters swayed by environmental considerations, the “cool factor” of the vehicles and government incentives. While EVs gain market share, some incumbent automakers have signaled caution about broader consumer acceptance, and stakeholders are increasingly aware of the lingering challenges of affordability and ease of public charging. An S&P Global Mobility consumer survey corroborates such caution: The proportion of consumers in key global auto markets open to purchasing an EV dropped to 67% in 2023, from 71% in 2022 and 86% in 2021.

EVs generally remain more expensive than conventional internal combustion engine vehicles. In Europe and the US, this is compounded by cost-of-living concerns and higher interest rates, both of which are impacting the broader automotive market. This is one example of the link between macroeconomic conditions and the pace of the energy transition.1

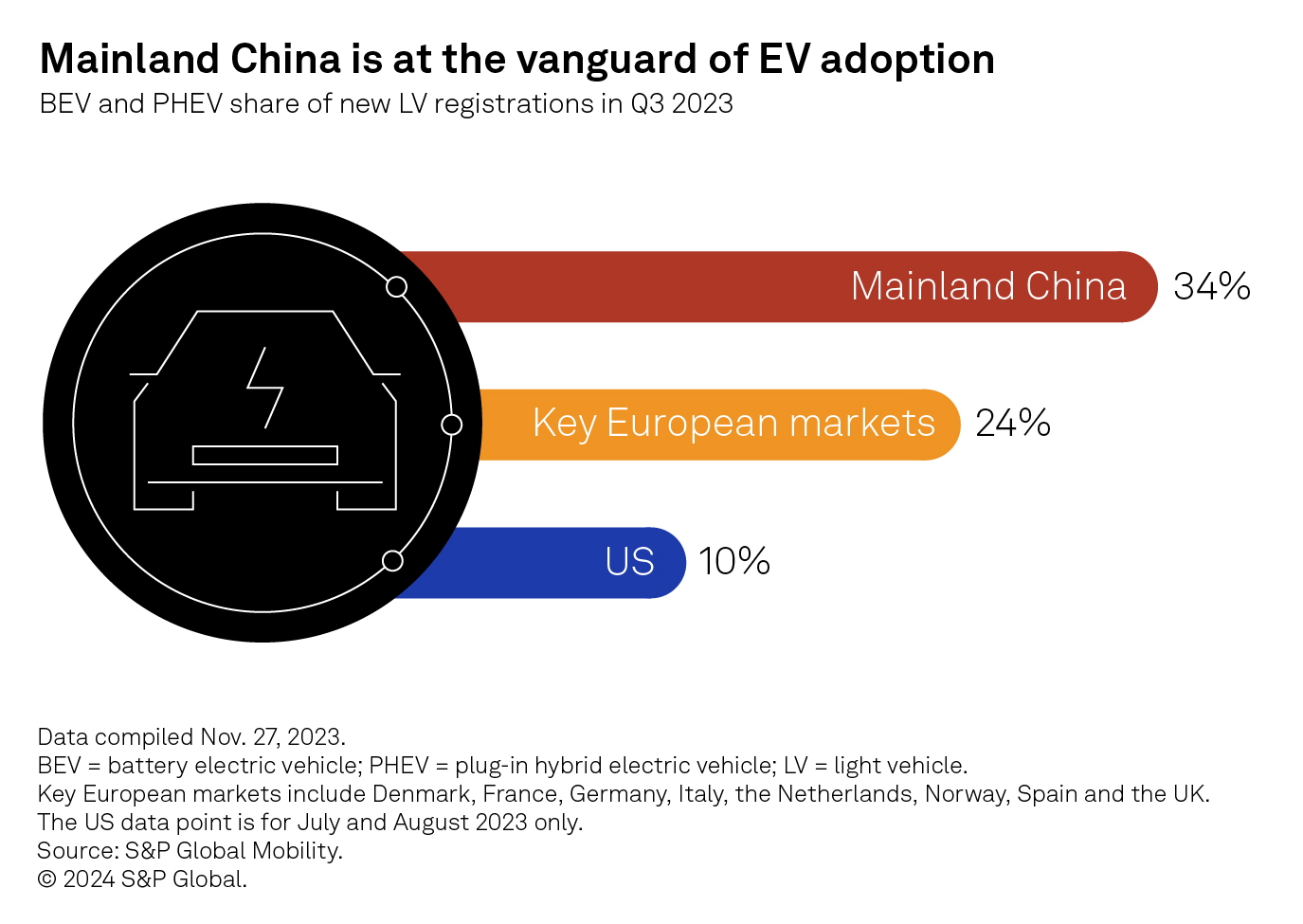

Mainland China, the epicenter of the global battery supply chain, is an exception, where EVs are increasingly attracting mainstream car buyers. In the third quarter of 2023, battery-electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) accounted for 34% of new light-vehicle (LV) registrations, supported by the availability of many competitively priced, software-rich EVs and the rapid expansion of public fast-charging infrastructure.

Government policy is an important driver of EV adoption. Increasingly stringent carbon dioxide and zero-emission vehicle (ZEV) sales requirements for automakers, coupled with EV purchase incentives for consumers, are supporting EV adoption from the supply and demand sides, respectively.

Key policies include the EU’s CO2 regulation for LVs, which requires automakers to cut CO2 emissions by 100% by 2035; California’s ZEV mandate, which requires automakers to sell 100% light ZEVs, also by 2035; and the US Inflation Reduction Act, which includes generous tax credits for battery production and for new and used EV purchases, albeit with income, vehicle price and supply chain country of origin restrictions.

Such policies compel automakers to develop and bring to market more, and more affordable, EVs and offer consumers help in bridging the near-term price gap.

It is unclear whether there will be enough battery raw materials to produce the number of EVs the industry plans to build over the next decade. This is a risk to steep EV adoption. New supply of battery minerals can be subject to long lead times, and market tightness could apply upward pressure on prices and make BEVs more expensive.

At the same time, battery security is becoming a greater focus for both governments and industry. Parts of the battery supply chain are highly geographically concentrated, notably mineral processing capacity in mainland China, adding another layer of supply risk.

Lithium is the building block of lithium-ion batteries. Spot lithium prices surged more than 500% between June 2021 and December 2022 before falling by about 70% by October 2023 (see chart). S&P Global Commodity Insights forecasts lithium supply to outpace demand over the next few years, owing in part to a supply response to the much higher prices of 2021–2022. In the latter part of the decade, the lithium supply-demand balance could tip into a sustained deficit as a potential sharp rise in EV-driven demand overtakes supply. Supply of other key battery raw materials, such as cobalt and nickel, could also fall short of demand later this decade, putting upward pressure on their prices.

Yet a sustained period of high battery raw material prices is not inevitable. If the history of the markets for these and other commodities is a guide, their prices will be cyclical, with high and low prices prompting responses from both the supply and demand sides.

For example, novel lithium extraction methods, such as direct lithium extraction, could increase lithium output. Greater adoption of lower-cost, though less energy dense, alternatives to nickel-rich battery chemistries could moderate the impact of higher mineral prices on battery costs (see chart). These alternatives include lithium-iron-phosphate and lithium-manganese-iron-phosphate chemistries, neither of which use cobalt and nickel, and sodium-ion, which does not use lithium. Battery-makers’ claims of energy density breakthroughs should be treated with caution, but solid-state battery technologies could offer a step-change in energy density, enabling a much-improved combination of driving range and cost compared with incumbent lithium-ion battery technologies.

As with other commodities, the prices of battery minerals will fluctuate, and automakers may adjust their product offerings and pricing to manage periods of higher battery costs as they strive to meet increasingly stringent government regulations.

S&P Global Mobility expects the global EV share of LV sales to rise to between 39% and more than 50% in 2030, from an estimated 17% in 2023. The range reflects multiple plausible outcomes based on differences in assumptions including regulatory stringency, consumer acceptance (including driving range) and battery costs. The pace of EV adoption will differ by region, with Europe and mainland China set to be at the forefront among large auto markets, followed by the US. In most emerging market economies, such as India, adoption is expected to be slower, owing to vehicle affordability and power infrastructure challenges, although lower-priced Chinese EVs could accelerate adoption in price-sensitive markets.

The pace of EV adoption will differ by region, with Europe and mainland China set to be at the forefront among large auto markets, followed by the US.

Tension between tighter regulations and consumer acceptance of EVs is likely to continue generating turbulence for the businesses of incumbent automakers. Ultimately, a widening gap between auto industry investments in EVs and internal combustion engine (ICE) vehicles means that technology and economies of scale will improve faster for the former, trends that will whittle down the “BEV premium” for prices.

Over time, EVs will erode oil’s near-monopoly as a road transportation fuel.

In a notable inflection point, the global fleet of light conventional ICE vehicles is expected to peak in the next few years and begin to gradually decline. A peak in global LV gasoline and diesel demand is likely to be roughly concurrent with a peak in the conventional ICE vehicle fleet.

In one gauge of the impact of EV penetration on oil demand, by 2030, EVs could displace more than 3 million barrels per day of oil demand in the Mobility and Energy Future service’s base case, on top of the volumes displaced by continued improvements in fuel economy of conventional ICE vehicles.

Just a few years ago, energy circles suggested that destruction of oil demand by EVs was a challenge for the “next decade.” Yet policy, industry and market developments have since accelerated the timeline by which the impact of EVs on oil consumption is likely to be felt.

For major oil importers such as mainland China and India, adoption of EVs will have a moderating influence on their oil import dependency ratios and, in turn, the scale of their broader energy import outlays. This dynamic will play out over decades, even in an accelerated EV transition scenario, and oil will prove particularly difficult to dislodge from other sectors of the world economy, including aviation and petrochemicals.

Affordability tops charging and range concerns in slowing EV demand

Mainland Chinese consumers crossing the chasm to mainstream EV adoption

Charging infrastructure incentives gain momentum in key EV markets

Next Article:

The challenges of aging: Fast and slow

1In this article, EVs refers generally to battery-electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs) and fuel-cell electric vehicles (FCEVs). Conventional internal combustion engine (ICE) vehicles are considered to be all other powertrain types. Like BEVs, PHEVs can be plugged in but have both an ICE and a battery. Many consider PHEVs to be a “bridging” technology between ICE vehicles and BEVs. Light vehicles (LVs), which include passenger cars and light trucks, are the focus of this article. Medium and heavy vehicles (MHVs) are also a priority for policymakers seeking to reduce transportation sector emissions, although the market for zero-emission MHVs is at an earlier stage of development than for LVs.

This article was authored by a cross-section of representatives from S&P Global and in certain circumstances external guest authors. The views expressed are those of the authors and do not necessarily reflect the views or positions of any entities they represent and are not necessarily reflected in the products and services those entities offer. This research is a publication of S&P Global and does not comment on current or future credit ratings or credit rating methodologies.